What is the 30% Rule to Avoid Becoming House Poor?

May 1, 2025 | 10:41 AM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

The views and opinions expressed in this editorial are those of the writer’s and do not necessarily reflect the views or positions of Pattison Media.

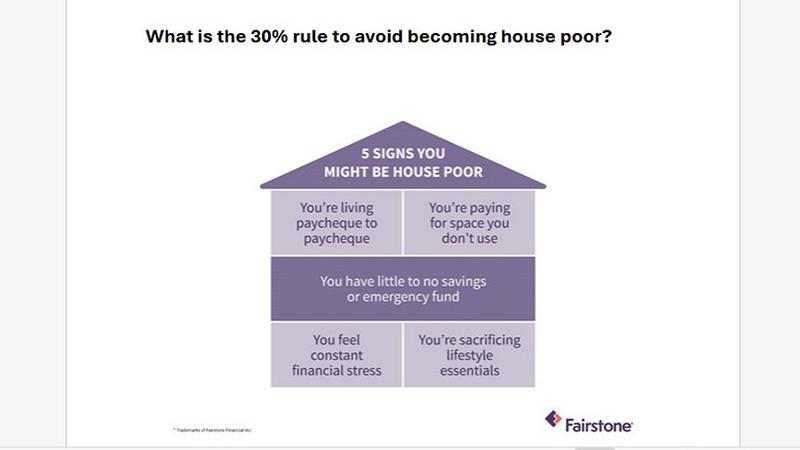

5 signs you might be house poor

When deciding how much house you can afford, a common guideline is the 30% rule —your housing costs (including mortgage, property taxes and insurance) shouldn’t exceed 30% of your gross monthly income. If your housing expenses are above this threshold, you could be at risk of being house poor.

But being house poor isn’t just about dollars and cents — it’s also about the sacrifices and strain that can come with homeownership.